Copper, which is widely regarded as a leading

indicator for economic activity and therefore dubbed as the metal with a PhD in

economics, is down 12.5% since the end of 2012. Also other base metals have

lost in 2013 so far. All base metals reached their high of the year in

mid-February and then moved downwards. Thus, the testimony of Fed Chairman

Bernanke, where he indicated the FOMC might taper the bond buying program at

one of the next few FOMC meetings, could hardly explain the poor performance of

base metals. Institutional investors have sold base metals already before this

testimony in May.

In our fair value models, the US dollar index is also

one of the explanatory variables for the price development of base metals. As

many of the variables are not stationary and also show a seasonal pattern, the

year-over-year percentage change had been applied in the models. The strength

of the US dollar index following the change of economic policy in Japan

When the fair value models were developed, the S&P

500 Index was the stock market index with the best explanatory power among the

major stock indices. At this time, China US

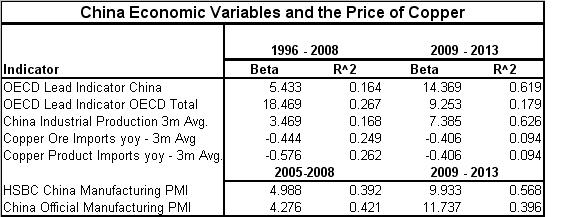

In many reports about the base metal markets, the

gradual decline of Chinese GDP growth is often cited as a reason for weaker

base metal prices. Therefore, we examined various Chinese macroeconomic

variables whether they explain the development of the 3mth LME copper price

better than they did before. In order to have enough observation also in the

second subsample, the starting date for the second sample had been set to

January 2009. However, in 2009 and also for most part of 2010, the development

of Chinese leading economic variables and international leading indicators was

very similar.

As the interest was only in the explanatory power of

some macroeconomic variables for the development of the copper price, we

estimated only some bivariate linear regression models instead of multivariate

models.

When we developed our fair value models for the base

metal prices, the OECD leading indicator for the total OECD explained the

development of copper prices better than the OECD leading indicator for China China China

A similar development took place for the industrial

production in China

One would assume that Chinese copper imports would

play an important role for the copper price. Many analysts had presented charts

showing the LME copper price being highly correlated with Chinese copper

imports. However, those analysts manipulated the charts in their studies

because they showed copper imports in value terms. And it is quite natural that

the copper price is highly correlated with the product of copper prices and

imported volumes. But looking at Chinese copper imports in volume terms shows a

different picture. The regression coefficient for copper ore imports as well as

for copper product imports (also smoothed by a 3mth moving average) is negative.

A possible explanation for this negative relationship might be that the more

copper China

Manufacturing PMIs for China

Chinese macroeconomic variables have a stronger impact

on copper prices after the financial crisis than they had before the collapse

of Lehmann Brothers. But China China

Obviously, Dr. Copper moved to China USA is

still the second top copper consumer and the US China

No comments:

Post a Comment