Gold rose further

this past week and reached a high at 1,347$/oz. However, it seems that the rise

was not driven primarily by the movement of the gold forward rates or the gold

lease rates. The 1 month gold forward rate increased from -0.078 to -0.053%

while the 1 month gold lease rate came down from 0.269 to 0.240%. Moreover, the

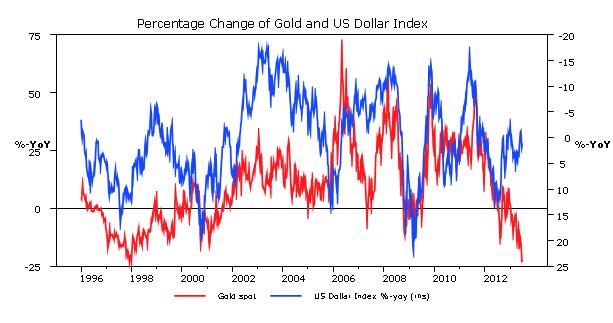

major fundamental factor driving gold higher was the US dollar. The US dollar

index weakened from 82.623 to 81.656. For the coming week, the US dollar might

remain the decisive factor for gold and other precious metals.

The focus in the

coming week is on the central bank policy in Europe with the ECB and the Bank

of England holding rate setting meetings as well as on the manufacturing PMIs

for various countries. And as usual at the first Friday of a new month, the US

labor market report will be released.

When the minutes of

the latest meeting of the BoE’s monetary policy committee (MPC) had been

released, many analysts were disappointed that the MPC decided unanimously to

keep the volume of bond holdings unchanged. However, such a result should not

come as a surprise. It was the first meeting under the new BoE Governor, Mike

Carney. For the two members, who voted for further bond buying, it would not be

a wise to oppose the position of the new BoE Governor. Voting with the majority

had not changed the result of a vote, but with joining the majority, they

demonstrate support for Mr. Carney. Also for Mr. Carney, it was smart to vote

with the majority. Voting for more quantitative easing and thus, against the

majority, could have been interpreted easily as a defeat damaging his

reputation.

However, more

important than the actual policy decision was the medium-term guidance, which

the BoE gave. Thus, monetary policy remains accommodative, but appears less

likely that the MPC will vote next Thursday for further QE measures. The

preliminary GDP figures for the second quarter, showing an increase of 0.6%

over the first quarter, have reduced the likelihood for further stimulus measures.

At the latest press

conference, also the ECB provided the financial markets with a medium-term

guidance. ECB president Draghi stated that rates would be at the current or a lower

level for an extended period of time. Thus, the kept the door for a further

rate cut open. However, also at the forthcoming ECB council meeting a rate cut

appears as less likely for two reasons.

First, council

members from the Northern Eurozone periphery already opposed a further rate cut

at the latest meeting. Their opposition has probably not weakened over the last

few weeks. There might be a slight majority in the council for a cut of the key

refinancing rate to 0.25%, however, the ECB council is looking for a broad

consensus for policy measures. The status quo will probably prevail at least

for another month.

Second, the flash

estimate of the Eurozone manufacturing PMI shows a reading of 50.1. It is the

first time since July 2011 that the manufacturing PMI would be above the

critical threshold of 50 if confirmed by the final figure. In Spain, the

unemployment rate declined for the first time since 2008, which is another

indication that the economic situation in the Eurozone recovers gradually. The

ECB always expressed the expectation that the Eurozone economy would improve in

the second half of this year. Therefore, it is more likely that the council

will take a wait and see attitude and keeps the powder dry.

For the US labor market

report, the consensus is looking for a slightly slower pace of new job creation

and predicts 180,000 (after 195K in June) additions to the payroll. The

unemployment rate is expected to decline to 7.5% from 7.6%. Thus, the

percentage of Wall Street economists predicting that the Fed would start

tapering the bond purchases at the September FOMC meeting could increase.

For the government

bond markets, these developments would be negative. The markets already reacted

on the better than expected economic figures in the UK and the Eurozone.

However, keeping the monetary policy unchanged by both central banks could

dampen hopes for more monetary stimulus further and could lead to another round

of bond selling. Whether the yield spread of 10 year US Treasury notes over

German Bunds will decline further depends crucially on the US labor market

report. A strong report could lead to a renewed spread widening. Higher bond

yields are expected to have a negative impact on the precious metals as they

imply higher opportunity costs.

The impact on the US

dollar is not so clear. Unchanged monetary policy in Europe would be normally

negative for the US dollar. However, a strong US labor market report could give

the US dollar a push as the market would probably price in a higher likelihood

for tapering at the September FOMC meeting. Nevertheless, even with a strong US

labor market report, the euro might hold well against the US dollar in the case

that the manufacturing PMIs for the Mediterranean countries also improve considerably.

Indications for economic improvement, in particular in Spain and Italy, would

reduce the credit risk of the government bonds, which should lead to narrower

spreads of the German Bunds as the Eurozone benchmark. Of course, the spread tightening

could be triggered by selling Bunds and buying Spanish or Italian government

bonds. But also investors, which have reduced their exposure in the Eurozone might

return as buyers if the economic outlook improves. This could support the euro

against the US dollar.

For the precious

metals, the US dollar index is more relevant than a single currency pair

according to our quantitative fair value models. Thus, a strong US labor market

report might be negative for precious metals by leading to a firmer US dollar

against the basket of five currencies in the US dollar index. Thus, we expect

that gold might end the coming week lower compared to the close of last Friday.

But a disappointing US labor market report might push gold above the 1,350$oz

level, which is regarded as a resistance level.