The slogan “it is the economy, stupid” is attributed

to Bill Clinton’s first presidential election campaign. For many market

participants, today’s version had to be “it is only the Fed, stupid”.

There is much discussion, especially in Germany

The best example for this unjustified believe were the

comments from some traders quoted by ThomsonReuters after the release of the

final figures of the PMI for the eurozone and some member countries. As the PMI

was slightly stronger than expected, bonds and stocks had been sold on

expectations that the ECB would end it expansionary monetary policy soon (see

also comment from Monday, July 1, 2013). But the eurozone is still in a recession and GDP

growth forecasts for the strongest economy, Germany, had been revised lower

lately by some institutions to a mere +0.3% in this year.

Unlike the Fed, the ECB has only a single mandate of

maintaining price stability. The ECB’s inflation target is to keep harmonized

CPI inflation close to but below 2% in the medium-term. This allows even for

some temporary overshooting of the target as long as the medium term inflation

outlook remains well anchored. But in a recessionary economic environment,

there is little underlying inflation risk. Thus, it is not rational expecting

the ECB to end the expansionary monetary policy only because some PMI figures

approach the 50 threshold.

Despite earlier comments from ECB president Draghi,

financial markets remained in irrational mode. This induced the ECB council to

send another clear message to financial markets. Breaking with the tradition of

stating that the ECB council is not pre-committed, the ECB council stated that the

key interest rates will stay at the current or lower level for an extended

period of time. But unlike the Fed, the ECB gave no clear guidance how long

this extended period will last. Questions during the press conference about the

duration were only answered by Mr. Draghi as “not 6 month, not 12 months, but

by an extended period”.

Similarly, it was also not rational to expect the BoE

to end expansionary monetary policy anytime soon. The MPC did not embark on

another round of bond purchases, but also did not send any indication there

might be a shift towards a restrictive policy. Thus, whether the statement made

by the BoE governor Carney was driven primarily by the change at the helm of

the institution or by the irrationality of financial markets is of minor

importance. What counts is the message

itself that monetary policy remains accommodative.

In the US

The FOMC statements always refer to the unemployment

rate as the second target and not to the non-farm payroll figure. Of course, a high

number of newly created jobs month after month are one important factor for

reducing the unemployment rate. But another important factor is the development

of the civilian workforce. In the second quarter, the workforce increased by more

than 800K to 155,835 thousand persons. In the quarters before, the workforce

declined as many persons unable to find a job left the workforce. With the

improved economic outlook, some of those leavers return again. This was the

reason that the unemployment rate remained unchanged at 7.6% despite more new

jobs than predicted had been created. It has to be expected that the increase

of the workforce is going to continue. This return to the workforce is

dampening the decline of the unemployment rate. But if the unemployment rate

remains at the current level, it gets less likely that the FOMC will vote for

reducing the volume of QE3. Whether job creation will be sufficiently strong to

reduce the unemployment rate over the summer months has to be seen. But that

the Fed enters tapering in September is not yet a done deal.

Thus, the outlook for monetary policy is divergence in

the direction. In Japan

After the release of the US

labor market report, the yield on the 10yr US

At the current level, 10yr US Treasury notes start to

get attractive for carry-trades. However, for financial institutions to enter

such trades, also the upside risk has to be limited. This is at present not the

case, as the uncertainty in the US Treasury market is likely to stay until the

FOMC has made a clear decision and does not only lay out the road map. Thus, we

still expect that yields on 10yr US Treasury notes could rise towards 3% before

stronger entering of carry trades sets in. This implies that the US dollar

could strengthen further against other major currencies.

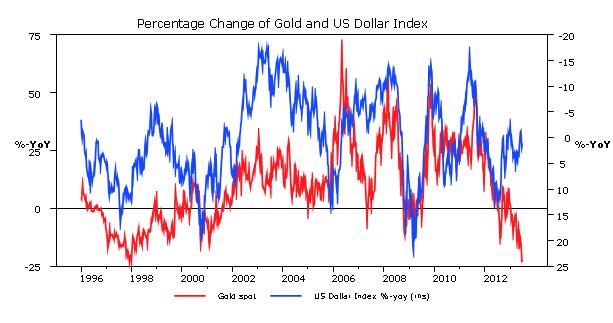

Last week, we pointed out that the negative link

between precious metals prices and the US dollar index remain well intact, but

that the regression coefficients between precious metals and the S&P index

as well as the US Treasury yield had reversed and became negative. Thus, a

further rise of US Treasury yields is likely to exercise two negative impacts

on the performance of precious metals, one directly and indirectly via the

foreign exchange markets and a rising US Dollar index. Thus, also the third

quarter, which just started, appears to be a negative on for the precious

metals.

No comments:

Post a Comment